Moving to Canada with 529B plan

My husband and I recently moved to Vancouver from the U.S. to raise our twin daughters (they are two years old). The girls are American, but we are applying to get them dual citizenship which could take another year. I’m a Canadian and my husband is American. We started saving in the U.S. within a 529b plan, and would like to continue saving for our daughters’ education now that we live in Canada. Can we open up a joint, family RESP, or should we continue with the 529b plan?

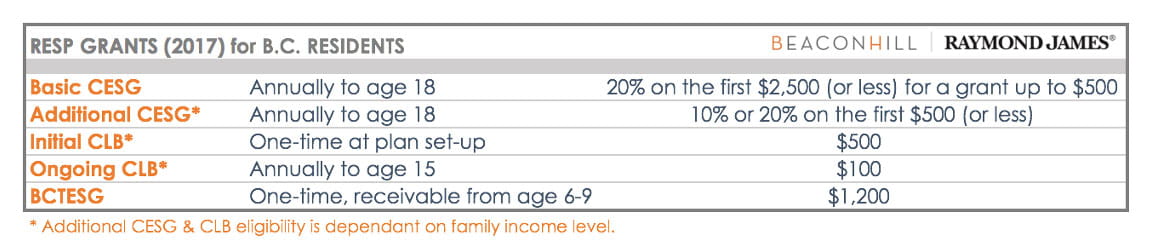

Now that you are residents of Canada, you can no longer contribute to your 529b plan. Opening up a registered education savings plan (RESP) is a fantastic way to start saving for a child’s post-secondary education in Canada. Funds invested in an RESP grow tax-deferred, and investment income will be taxed in the hands of the beneficiary child, at their applicable tax-rate, when withdrawn. There is also the benefit of Canadian Education Savings Grants (CESG) and Canada Learning Bonds (CLB). All Canadian resident children, regardless of citizenship, are eligible for the grants, so no need to wait for the girls to get their citizenship. The basic matching grant is 20% on the first $2,500 invested into the plan per child per year to age 18, with options for additional grants for lower income families. If you invest $5,000 per year in a family RESP for two children, you will get $1,000 in grants annually ($500 per child). As residents in the province of British Columbia (B.C.), you are also eligible for the one-time B.C. Training and Education Savings Grant (BCTESG) of $1,200 per child, for children born on or after January 1, 2006. You can apply for the grant from your twins’ sixth birthday up until the day they turn nine, but you will need to be a B.C. resident at the time the grant application is made.

With multiple children, a family RESP is a great option. While the grant monies received are specific to each child, the balance of the funds invested can be allocated amongst your children as needed, giving you and your family added flexibility over having multiple individual plans.

While many parents perceive this as a joint investment venture, having a joint RESP account with a U.S.-person (i.e. your American husband), poses several challenges. The Canadian RESP is not recognized under the Canada – U.S. Income Tax Convention, and therefore does not receive tax-deferred treatment for U.S. tax purposes. The investment income will be taxable in the year received to your husband, and again in the future when your children withdraw the funds, opening up the possibility of double taxation. Although you are a Canadian citizen, if you took up permanent residence and a green card while living in the U.S., you could also be considered a U.S.-person, and therefore subject to the same taxation challenge. Additionally, the RESP account could be considered a foreign trust by the IRS, requiring annual filing of forms 3520 and 3520A. The additional accounting costs could quickly erode the benefit of the grants. The solution is to have a non-US person open the account for your daughters (i.e. a Canadian grandparent, aunt, uncle, etc.). Whoever opens the account is referred to as the subscriber, and funds invested into the RESP, with the exception of the grants, become an asset of the subscriber. It is therefore important to select an individual whom you trust won’t run off the funds.

Unlike the Canadian RESP program, which is federal, the U.S. equivalent 529 plans (also called a qualified tuition program or QTP) are run by each state or even at the college level, and the terms and benefits of these accounts vary greatly. The allowable contributions far exceed that for the RESP, but investment options are limited. Not all plan administrators will allow non-residents to hold 529 plans, so you may be required to move the plan via a rollover. Note that only one rollover is allowed in any 12-month period. Many families elect to simply use the address of a relative in-state to avoid the hassle of a rollover, but it’s easy enough to move a plan, and if your administrator insists you move, there should be no cost for you to do so. However, if you received a tax deduction for contributions, the state may require you to pay income-tax on those contributions if the plan moves out of state. The U.S. based 529 plans cannot be rolled into a Canadian RESP, and will have to remain as a separate plan. While investments in 529 plans grow tax-free and are exempt from federal tax in the U.S., the same does not apply in Canada and the CRA provides no exemption or deferral of taxation for income earned or distributed on a 529 plan. Additionally, if the donor is a resident of Canada, the 529 plans could be considered a deemed resident trust or an offshore investment fund property, requiring inclusion in the annual filing of form T1135, foreign income verification statement, if the 529 plan, along with your other specified foreign property has a cost in excess of $100,000 CAD. Given that your daughters are only now two years of age, and assuming the balance of the 529 plan is small, you should discuss with your tax counsel if there is any benefit to keeping the plan as a resident of Canada, since Canadian residents potentially lose all the tax advantages of the plan. You would owe income tax (potential recouped as a foreign tax credit), as well as a 10% early withdrawal penalty (non-recoverable), but the funds could then be directed into a Canadian RESP (with a Canadian subscriber) with the benefit of the 20% CESG, no need for additional filing, and tax advantaged treatment of income going forward.

Both the U.S. 529 plans and the Canadian RESP offer great options to save for a child’s post-secondary education. Which plan is the right plan for your family going forward, and how to manage or amend existing plans when you move across a border require careful planning. Every situation is different, and detailed consultation with both your investment and tax advisors will ensure that your family can most efficiently plan for the future.

Dixie Klaibert, CFA®, is a financial advisor with both Raymond James Canada and Raymond James (USA) Ltd. She is a branch manager of Beacon Hill Wealth Management, an independent office of Raymond James Ltd (Canada). She specializes in cross-border asset management and financial advisory.

The views of the author do not necessarily reflect those of Raymond James. This article is for information only. Raymond James Ltd. member of Canadian Investor Protection Fund.Raymond James (USA) Ltd. member FINRA/SIPC. Raymond James (USA) Ltd. is a wholly owned subsidiary of Raymond James Ltd. Information in this article is from sources believed to be reliable; however, we cannot represent that it is accurate or complete. It is provided as a general source of information and should not be considered personal investment advice or solicitation to buy or sell securities. The views are those of the author, Dixie Klaibert, and not necessarily those of Raymond James Ltd. Investors considering any investment should consult with their investment advisor to ensure that it is suitable for the investor’s circumstances and risk tolerance before making any investment decision. Raymond James Ltd. is a Member Canadian Investor Protection Fund.

Website legal disclaimers

Raymond James Ltd. is an indirect wholly-owned subsidiary of Raymond James Financial, Inc.

Securities-related products and services are offered through Raymond James Ltd., member Canadian Investor Protection Fund.

Insurance products and services are offered through Raymond James Financial Planning Ltd, which is not a member Canadian Investor Protection Fund.

Raymond James Trust Services are offered by Raymond James Trust (Canada) in the provinces of British Columbia, Alberta, Saskatchewan, and Ontario, and by Raymond James Trust (Québec) Ltd. in the province of Québec. Both entities are wholly owned subsidiaries of Raymond James Ltd. Trust Services are not covered by the Canadian Investor Protection Fund.

Use of the Raymond James Ltd. website is governed by the Web Use Agreement | Client Concerns.

Website legal disclaimers

Raymond James Ltd. is an indirect wholly-owned subsidiary of Raymond James Financial, Inc.

Securities-related products and services are offered through Raymond James Ltd., member Canadian Investor Protection Fund.

Insurance products and services are offered through Raymond James Financial Planning Ltd, which is not a member Canadian Investor Protection Fund.

Raymond James Trust Services are offered by Raymond James Trust (Canada) in the provinces of British Columbia, Alberta, Saskatchewan, and Ontario, and by Raymond James Trust (Québec) Ltd. in the province of Québec. Both entities are wholly owned subsidiaries of Raymond James Ltd. Trust Services are not covered by the Canadian Investor Protection Fund. Use of the Raymond James Ltd. website is governed by the Web Use Agreement | Client Concerns.

Raymond James (USA) Ltd. All rights reserved.

Raymond James (USA) Ltd. advisors may only conduct business with residents of the states and/or jurisdictions in which they are properly registered. Investors outside the United States are subject to securities and tax regulations within their applicable jurisdictions that are not addressed on this website.

Raymond James (USA) Ltd. is a member of FINRA/SIPC.

![]()

This website may provide links to other internet sites for convenience of users. Raymond James (USA) Ltd. is not responsible for the availability of content of these websites, nor does the firm endorse, warrant or guarantee the products, services, or information described or offered by these other internet sites. Users cannot assume that these websites will abide by the same Privacy Policy that Raymond James (USA) Ltd. adheres to.