Foreign withholding taxes on US securities

The hidden cost of foreign withholding tax

Just beneath the surface...

Investors today have rightly been focused on keeping an eye on their investment costs. Numerous studies have shown that keeping investment cost low is one of the best indicators of future success. Investors only keep net returns (returns after costs and taxes), and can increase returns by making sure they have the right investment structure to reduce any unnecessary double taxation.

The tectonic shift from high cost investing to low cost investing has been the single most disruptive change the industry has ever faced. Over $650 Billion dollars flowed out of high cost funds in 2017 alone, to companies like Vanguard, BlackRock (iShares) and Dimensional.

This flow of funds is expected to continue in the coming years, albeit at a slower pace here in Canada for reasons we touched upon in a previous article.

Like beauty, MER is only skin deep

Most investors look to MER as a reflection of their total costs. It can be misleading when other hidden costs can equally impact investor performance.

One of the least understood and hidden costs is foreign withholding tax. The tax is incurred when an investor in Canada receives dividends from non-Canadian investments such as US or foreign stocks. Most countries require tax to be withheld from dividend payments to foreign investors (Canadians in this case). This tax varies by country, but 15% is the most common rate.

Taxable investors in Canada can receive a credit for the amount of foreign taxes paid (up to 15% of dividends), so the tax paid to foreign governments is substantially, if not completely offset by a reduction in Canadian taxes. Note, in registered plans (RRSP, RIF, TFSA), investors do not receive a refundable credit.

How these foreign securities are held (directly or indirectly) in Canada becomes critical in reducing the tax drag of different layers of foreign withholding tax.

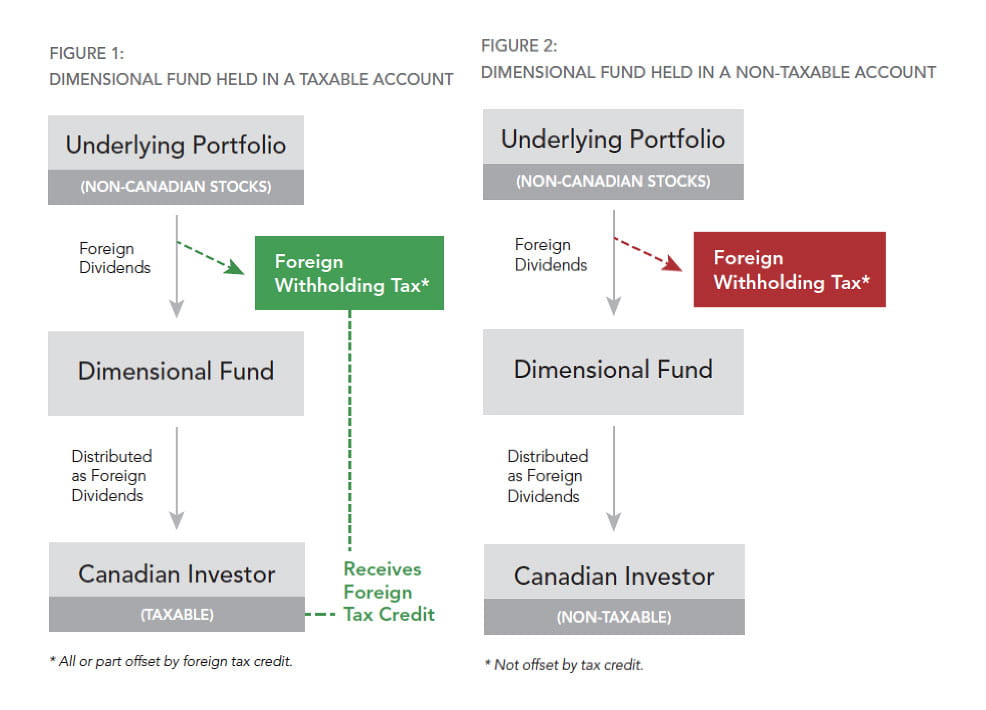

Foreign Securities Held Directly in Canada

Figures 1 & 2 below illustrate how foreign dividends flow to investors in a Canadian-domiciled fund that directly holds the shares of non-Canadian dividend paying securities in both a taxable and non-taxable account. In both cases the fund delivers the dividends paid to investors. In the case of the taxable investor, the foreign tax withheld is offset by the tax credit received (highlighted in green). In non-taxable (registered) accounts, there is no offsetting credit received (highlighted in red)

Foreign Securities Held Indirectly in Canada

The foreign withholding tax gets more complicated and opaque once the securities are held indirectly. Indirectly holding the securities most commonly occurs two ways.

- When a Canadian investor holds a US listed ETF (exchange traded fund) that holds non-US securities like European or Emerging Market stocks. The sheer volume, selection, and lower cost of US listed ETFs dwarfs what is available here in Canada, and are popular choice for investors.

- When a Canadian investor holds a “wrapped” Canadian listed ETF. An example of this would be a Canadian listed emerging market ETF that holds the corresponding US listed emerging market ETF with a currency hedge. These are used by Canadians to get the emerging market exposure offered on the US listed version, but in CAD$.

Chris Stooksbury, is a financial advisor with both Raymond James Canada and Raymond James (USA) Ltd. He specializes in cross-border asset management and financial advisory.

The views of the author do not necessarily reflect those of Raymond James. This article is for information only. Raymond James Ltd. member of Canadian Investor Protection Fund.Raymond James (USA) Ltd. member FINRA/SIPC. Raymond James (USA) Ltd. is a wholly owned subsidiary of Raymond James Ltd. Information in this article is from sources believed to be reliable; however, we cannot represent that it is accurate or complete. It is provided as a general source of information and should not be considered personal investment advice or solicitation to buy or sell securities. The views are those of the author, Chris Stooksbury, and not necessarily those of Raymond James Ltd and Raymond James (USA) Ltd. Investors considering any investment should consult with their investment advisor to ensure that it is suitable for the investor’s circumstances and risk tolerance before making any investment decision.

Website legal disclaimers

Raymond James Ltd. is an indirect wholly-owned subsidiary of Raymond James Financial, Inc.

Securities-related products and services are offered through Raymond James Ltd., member Canadian Investor Protection Fund.

Insurance products and services are offered through Raymond James Financial Planning Ltd, which is not a member Canadian Investor Protection Fund.

Raymond James Trust Services are offered by Raymond James Trust (Canada) in the provinces of British Columbia, Alberta, Saskatchewan, and Ontario, and by Raymond James Trust (Québec) Ltd. in the province of Québec. Both entities are wholly owned subsidiaries of Raymond James Ltd. Trust Services are not covered by the Canadian Investor Protection Fund.

Use of the Raymond James Ltd. website is governed by the Web Use Agreement | Client Concerns.

Website legal disclaimers

Raymond James Ltd. is an indirect wholly-owned subsidiary of Raymond James Financial, Inc.

Securities-related products and services are offered through Raymond James Ltd., member Canadian Investor Protection Fund.

Insurance products and services are offered through Raymond James Financial Planning Ltd, which is not a member Canadian Investor Protection Fund.

Raymond James Trust Services are offered by Raymond James Trust (Canada) in the provinces of British Columbia, Alberta, Saskatchewan, and Ontario, and by Raymond James Trust (Québec) Ltd. in the province of Québec. Both entities are wholly owned subsidiaries of Raymond James Ltd. Trust Services are not covered by the Canadian Investor Protection Fund. Use of the Raymond James Ltd. website is governed by the Web Use Agreement | Client Concerns.

Raymond James (USA) Ltd. All rights reserved.

Raymond James (USA) Ltd. advisors may only conduct business with residents of the states and/or jurisdictions in which they are properly registered. Investors outside the United States are subject to securities and tax regulations within their applicable jurisdictions that are not addressed on this website.

Raymond James (USA) Ltd. is a member of FINRA/SIPC.

![]()

This website may provide links to other internet sites for convenience of users. Raymond James (USA) Ltd. is not responsible for the availability of content of these websites, nor does the firm endorse, warrant or guarantee the products, services, or information described or offered by these other internet sites. Users cannot assume that these websites will abide by the same Privacy Policy that Raymond James (USA) Ltd. adheres to.